How to Enable Data-driven Innovation for the Mobility Insurance – Grape Up

Digitalization has changed the way we shop, work, learn and take care of our health or travel. Cars are no longer used just to get from A to B. They are jam-packed with technology that connects us to the world, enhances safety, prevents breakdowns, and even provides entertainment. With the rise of the Internet of Things and artificial intelligence, a vehicle is no longer understood solely in terms of its performance and sleek design. It has become software on wheels, a gateway to new worlds – not just physical, but also virtual. And if the nature of insurance itself is changing, then the company offering insurance must keep up with these changes as well. Insurance needs digital innovation, as much as any other market area.

These days customers are looking for customization, personalization, and understanding their needs on an almost organic level. Data and advanced analytics allow us to effectively satisfy these needs. Thanks to them, it is possible to fine-tune the offer, not so much for a specific group, but for a particular person – their habits, daily schedule, interests, health restrictions, or aesthetic preferences. And in the case described by us – a person’s driving style and commuting patterns.

If you think about it, the insurer has the perfect tool in their hands. If they can tap into the potential of the software-defined vehicle and equip it with the right applications, there will be nearly zero chance of inaccurate insurance risk estimates. Data doesn’t lie and shows a factual, not imaginary picture of a driver’s driving style and behavior on the road.

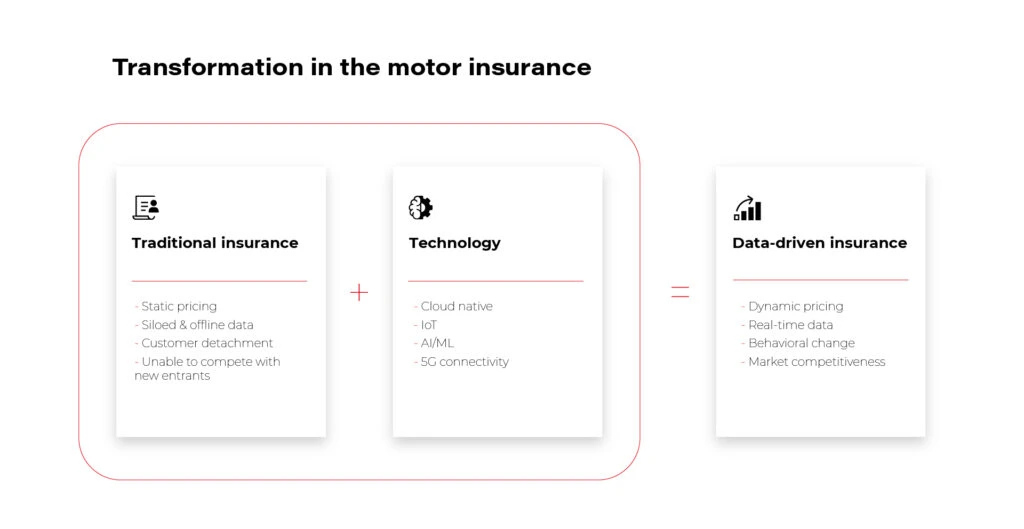

While in the traditional insurance model pricing is static and data is collected offline and not aligned with the driver’s actual preferences, new technologies such as the cloud, the IoT, and AI allow for these limitations to be effectively lifted.

With them, an offering is created that competes in the marketplace, generates new revenue streams within the company, and builds customer loyalty.

Data-driven innovation – easier said than done. Or maybe not?

The transformation of a vehicle from a traditionally understood mechanical device into a “smartphone on four wheels,” as Akio Toyoda once said about modern vehicles, takes time and will not happen overnight. But year by year it already happens, and as the new car models distributed by the big corporations show, this process is actually underway.

Read our article on the latest trends in the automotive industry

The so-called software-defined vehicle that we are developing with our clients at Grape Up is a vehicle that moves through an ecosystem of numerous variables, accessed by different players and technologies.

Clearly, one such provider can be – and should be – the insurer whose products have been tied to the automotive market invariably since 1897, when a certain Gilbert J. Loomis, a resident of Dayton, Ohio, first purchased an automotive liability insurance policy.

However, for insurance companies to play an integral role in the use of vehicle-generated data, the driver must receive a precisely functioning and secure service from which they will derive real benefits. Without building specific technical competencies and software-defined vehicle knowledge, the insurer cannot achieve these goals.

Only by creating this type of business unit from scratch in-house, or by partnering with software companies, will they be able to compete with insurtech startups like, e.g. Lemonade, which builds their businesses from the ground up based on AI and data analytics.

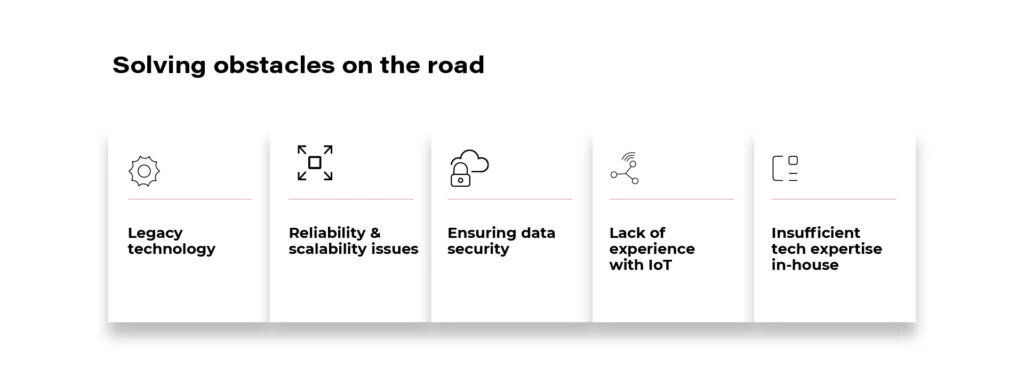

The right technology partner will take care of:

- data security;

- selection of cloud and IoT technologies;

- and will ensure the reliability and scalability of the proposed solutions.

During this time, the insurer can focus on what they do best – developing insurance competencies and tweaking their offers.

How to choose the right technology partner?

Just as customers are looking for insurance that accommodates their driving and lifestyle, an insurance company should select a technology partner that has more than just technical skills to offer. After all, changing the model in which a traditional insurance company operates does not boil down to creating a digital sales channel on the Internet and launching a modern website. We are talking about a completely different scale of operations requiring the insurance company to be embedded in a completely new, rapidly developing environment.

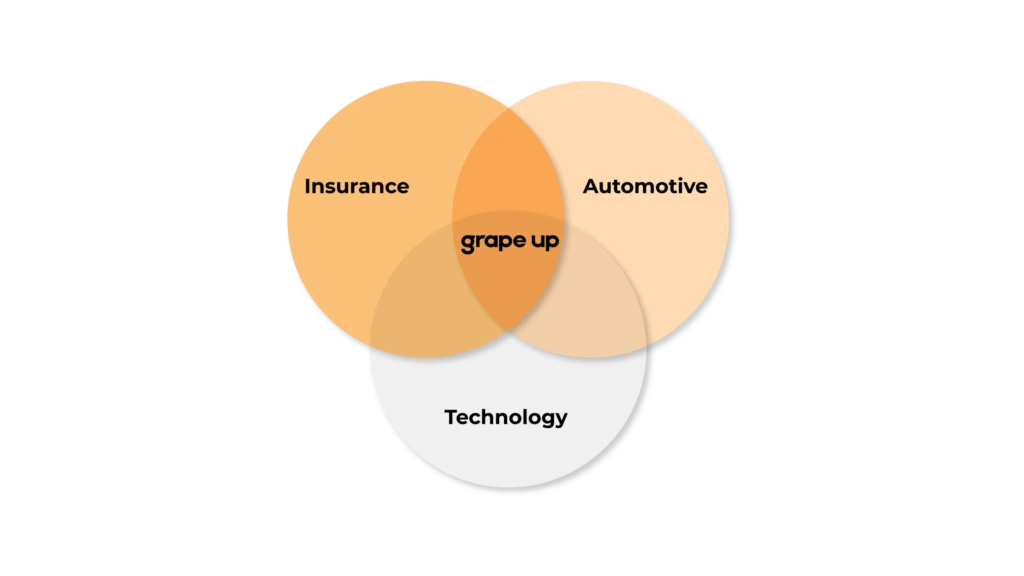

Therefore they need a partner who naturally navigates the software-defined vehicle ecosystem, understands its specifics, and has experience in working with the automotive industry. Besides, it should be someone knowledgeable about the specifics of the P&C insurance market and the challenges faced by the insurance client.

It is only at the intersection of these three areas: technology, automotive, and insurance, that competencies are built to effectively compete against modern insurtechs.

Like in the Japanese philosophy of ikigai, which explains how to find one’s sense of purpose and give meaning to one’s work, both companies can build valuable, useful solutions for users. They will bring satisfaction not only to customers but also to the insurance company, which will open a new revenue channel and meet the needs of the market.